Risk Rundown:

Remittance,

precious metals & cryptocurrency

Current fraud landscape

The rapid rise of neo-financial platforms and technology for remittance payments, precious metals trading, and cryptocurrencies has revolutionized money movement around the globe, providing unprecedented convenience.

In parallel, digitalization has paved the way for fraud, introducing new vulnerabilities that a diverse cast of fraudsters — from opportunistic amateurs to highly organized criminal networks — are eager to exploit. As money moves faster than ever, adopting innovative fraud prevention strategies is critical for financial players looking to balance risk and opportunity effectively.

TAKING STOCK

The value of remittances worldwide is expected to reach 913 billion U.S. dollars by 2025. The global market value of the precious metals gold, silver, and platinum amounted to a total of over 290 billion USD in 2022 and is forecasted to grow to over 500 billion USD in 2032. Over 10,000 cryptocurrencies exist nowadays, even if most have limited significance: Bitcoin and Ethereum account for nearly 75 percent of the entire crypto market capitalization.

A magnet for cybercriminals

Beyond their widespread consumer adoption, alternative financial services present an enticing opportunity for a spectrum of bad actors. With their global reach and rapid transactions offering near-instant delivery of value, many of these platforms offer ideal monetization channels for fraudsters looking to cash out their illicit proceeds.

Criminals recruit money mules to help open accounts and launder proceeds from online scams and frauds or crimes like human trafficking and drug trafficking. Money mules add layers of distance between crime victims and criminals, making it harder for law enforcement to trace money trails accurately. Honing in on the psychological element, some money mules know they are supporting criminal enterprises, but others are unaware that they are helping criminals profit. The bad actors might be part of organized crime groups or could be running fraudulent “friends and family” schemes through peer-to-peer (P2P) payment services.

Beyond a tool, fraudsters also see these platforms as product targets. They attempt to exploit the ‘human’ element in the authentication chain and steal funds directly, either from the platform itself or its users, through phishing scams, account takeovers (ATOs), and other forms of social engineering that can lead to authorized push payment (APP) fraud.

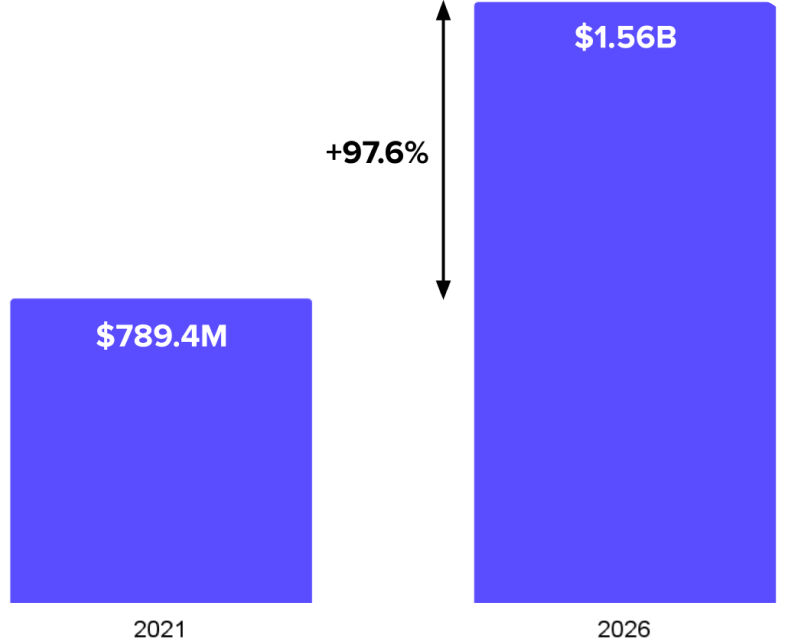

PROJECTED INCREASE IN APP FRAUD VOLUMES IN THE UK

Source: API Worldwide

Top trends to monitor

This section examines the common yet distinct fraud tactics Riskified sees within remittance payments, precious metals trading, and cryptocurrencies, offering insights into how bad actors target this high-value ecosystem.

First-time customers

As seen with its anticipated continued expansion, the alternative financial sector draws numerous new customers, which is vital for growth but fraught with challenges. From the extensive analysis of industry orders Riskified reviewed, first-time customers were potentially 40 times riskier than established customers with a 30+ day order history, making them a necessary but inherently risky segment for financial players.

NEW CUSTOMER SEGMENTATION

Total population

Fraudulent population

Global crises, fluctuations in exchange rates, and cryptocurrency booms, like the recent surge in Bitcoin, further heighten risks in the financial landscape. Increased activity provides opportunities for fraudsters to conduct high-velocity, low-value transactions because they know that fraud detection systems may struggle to keep pace with the overwhelming volume of orders.

Fraud ring foiled

A crypto merchant experienced a sudden surge in transaction volume. Initially, the increase seemed to be driven by first-time customers. Within just a few days, they had placed transactions worth over $220K. Key indicators included AVS-mismatched credit cards, either placing deposits or purchasing Bitcoin. Riskified identified these patterns as part of a larger fraud ring and declined all related transactions, leaving legitimate customers unaffected. After a few days, the fraudsters abandoned this tactic.

Cash-out fraud

Riskfied’s analysis of industry orders shows that fraudsters cash out from both new and existing accounts with legitimate online and offline histories. In account takeover (ATO) cases, the fraudster gains unauthorized access to an existing account. The account holder is unaware that their credentials are being used, but we can identify ATO cases because of a change in behavior based on the online and offline history of the customer.

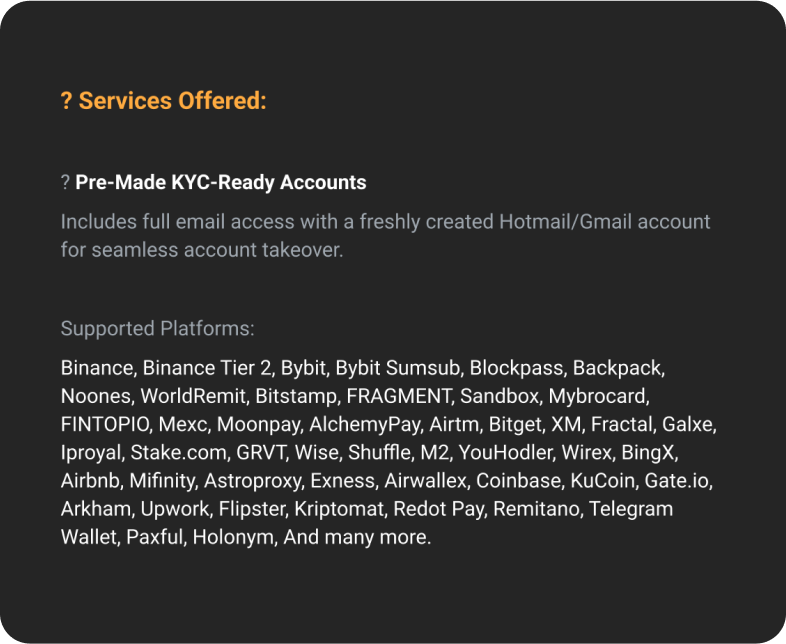

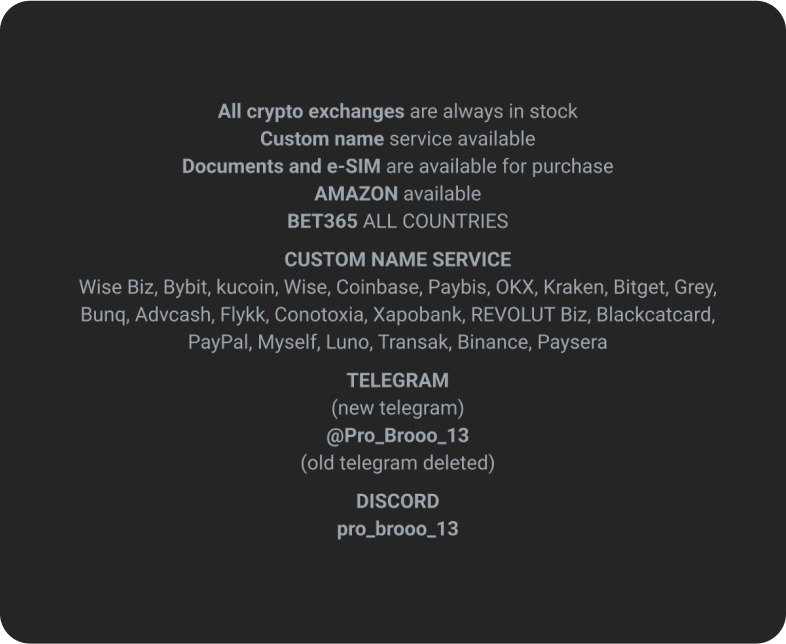

Alternatively, fraudsters highly value KYC-verified accounts due to the money exchanges' requirements for ‘Know Your Customer’ (KYC) identity verification checks. Nowadays, they are readily available in various dark web marketplaces. And due to the high demand, fraud-as-a-service providers also offer services like registering an account under a custom name, passing selfie verification, and providing any necessary documentation.

Proven strategies

Alternative financial services merchants need agile, intelligent fraud prevention strategies that can quickly adapt to the fast-growing payment markets.

Tap into a network of intelligence

To thrive in such dynamic conditions, businesses must ensure that the benefits of attracting new customers outweigh the inherent risks. By analyzing different account types — first-time, new, and established — across legitimate and fraudulent transactions, they can better understand the unique challenges posed by each segment and tailor their risk management strategies accordingly.

An efficient approach is to cross-reference every new order with a large dataset of past transactions from a global merchant network. A customer new to a platform may have a history with another merchant, revealing positive or negative signals that help paint a clearer picture.

71%

of customers new to cryptocurrency businesses were already part of the Riskified network

56%

of customers new to remittance businesses were already part of the Riskified network

74%

of customers new to precious metals businesses were already part of the Riskified network

Adopt adaptive strategies

As outlined above, fraudulent money orders are often executed in ways that mimic legitimate transactions. Detecting masking tactics, such as the use of a proxy, is crucial for separating genuine transactions from fraudulent ones. Effective fraud prevention systems should also leverage anomaly detection to uncover irregular patterns.

Furthermore, robust identity clusters are an important method of identifying and blocking illegitimate orders. This requires a broad network of data with customer orders and claims across accounts and merchants, advanced machine learning models, and a clustering strategy for identity resolution and risk evaluation.

Partner with Riskified

Unleash growth with solutions designed to safeguard what matters most — your customers, their transactions, and trust in your business.

About this Risk Rundown

Across industries, Riskified captures and analyzes data related to orders processed through our vast merchant network. We combine our findings with exclusive research and intelligence from online fraud forums to provide merchants with category-specific insights.

Yael Hemo

Data Analyst, Data Insights team