Risk Rundown:

Money movement

Current fraud landscape

The rapid rise of neo-financial platforms and technology for cryptocurrency, remittance payments, and precious metals trading has revolutionized money movement around the globe, providing unprecedented convenience and access, as well as new risks and vulnerabilities to fraud. What sets this industry apart is that the product itself is money — fraudsters no longer need to target high-value goods to profit; they now have direct access to the ultimate prize. This shift has not gone unnoticed by bad actors, who openly discuss and acknowledge the unique opportunities these markets present. The pace, liquidity, global scale, and somewhat uncharted nature of these platforms make fraud both appealing to commit and difficult to prevent.

What’s more, today’s scammers have more powerful tools than ever at their disposal thanks to AI and a growing global industry dedicated to committing and enabling financial fraud.

From opportunistic amateurs to industrial-scale scams run by organized criminal networks, fraudsters are racing to exploit the new frontiers of alternative finance. Many rely on phishing and other forms of social engineering to manipulate individuals, often leading to authorized push payment (APP) fraud, where victims are tricked into sending money to fraudulent accounts. Others bypass the need for human interaction entirely, using methods like account takeovers (ATOs), verification exploits, and circumventing know your customer (KYC) protocols to directly access and steal funds from platforms or users.

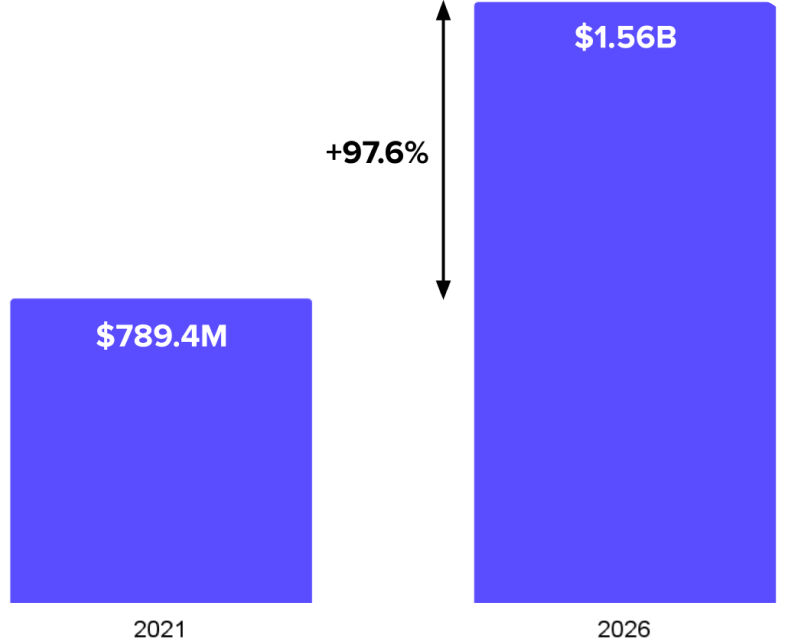

PROJECTED INCREASE IN APP FRAUD VOLUMES IN THE UK

Source: API Worldwide

Taking stock

There are an estimated 10,000 cryptocurrencies in circulation today in a $3 trillion market, with Bitcoin and Ethereum accounting for nearly 75 percent of the market cap. The value of remittances worldwide is expected to reach $913 billion in 2025, and the global market value of the precious metals market is forecast to grow to over $500 billion by 2032.

Unfortunately, fraud is bullish, too. Scammers stole an estimated $4.6 billion in crypto in 2024 alone, largely enabled by AI-generated deepfakes. In Japan, the amount of money lost due to online fraud has increased steadily: some confirmed cases had victims who were led to phishing websites via messages impersonating home delivery services and online shopping services. In some instances, fraudulent apps were installed on smartphones. Next to fraudulent remittances, methods involving crypto assets, electronic money, and the charging of prepaid cards were also confirmed.

Value of damages caused by online banking fraud in Japan from 2014 to 2023 (in billions)

Deloitte’s Center for Financial Services predicts industry fraud losses in the U.S. as high as $40 billion by 2027, with AI fueling much of the growth. In fact, “FinServ” or financial services fraud is so lucrative worldwide that it now has an entire services industry of its own.

Welcome to the age of ‘fraudserv’

Riskified analysts have observed a burgeoning dark-web business sector with the capacity to support fraud initiatives of any scale. This sector even comprises its own subsectors, such as fraudtech (voice cloning apps for sale), fraud-for-hire (phishing pros at your service), fraud data providers, and even recruiting campaigns feeding the fraud services ecosystem.

In this supply-and-demand marketplace, one can purchase AI tools and services for creating and streaming altered images, such as those for lifelike face-swapping, selfie-animation, voice cloning, caller-ID spoofing, and handwriting generation. Frauds-for-hire will perpetrate vishing or voice phishing on your behalf with convincing social engineering schemes. And data providers sell lead lists of desirable target groups, such as Binance or Coinbase users. These services are readily available and used to bypass even stringent KYC verification protocols in order to access or create financial accounts, digital wallets, and/or crypto.

AI and big-business fraud are driving up risk for financial players and platforms looking to balance risk and opportunity and stay agile despite these fraud factories. Legitimate financial service businesses must adopt innovative AI-resistant fraud prevention strategies that can adapt to this changing landscape while capturing as much business as possible in a growing market.

Top trends to monitor

This section examines the fraud tactics Riskified is seeing across cryptocurrency, remittance payments, and precious metals trading platforms, and how these platforms can protect themselves and their users.

First-time customers are risky but essential

Like any growth sector, alternative finance has a high proportion of new customers, which is vital for success but fraught with challenges. From an analysis of orders Riskified reviewed, first-time customers were potentially 40 times riskier than established customers with a 30+ day order history, making them a necessary but inherently risky segment for financial players. But fraudsters are also getting savvy; once they gain access to an account, they often wait to build trust, and then initiate fraudulent activities, making it even harder for fraud detection tools to identify patterns and mitigate risks effectively.

NEW CUSTOMER SEGMENTATION

Total population

Fraudulent population

Global crises, fluctuations in exchange rates, and cryptocurrency booms further heighten volatility and risks in the financial landscape. Increased activity provides opportunities for fraudsters to conduct high-velocity, low-value transactions because they know that fraud detection systems may struggle to keep pace with the overwhelming volume of orders.

FRAUD RING FOILED

In 2025, a crypto merchant experienced a sudden surge in new customer transactions purchasing Ethereum, and Riskified anomaly detection identified commonalities that signaled high risk. The transactions were all coming from Irish IP addresses, utilized similar payment methods and high transaction amounts, and had tell-tale signals of proxy connections. Initially, the increase seemed to be driven by first-time customers. Riskified quickly identified these high-risk patterns, enabling it to decline fraudulent transactions while leaving legitimate customers unaffected.

KYC verification fraud

Fraudsters highly value KYC-verified accounts because they bring with them a cloak of anonymity and legitimacy in the financial system, allowing fraudsters to conduct illegal activities without easy detection. Accessing these accounts is increasingly enabled by fraud-as-a-service providers that offer services such as registering an account under a custom name, passing selfie verification, and providing fake documentation, all using genAI tools to deceive KYC screening.

Cash-out fraud

Riskified’s analysis of fraud strategies discussed on the dark web and industry orders shows that fraudsters employ various methods to cash out funds. This includes taking over existing accounts (ATOs) — typically older accounts with legitimate online and offline histories — and draining balances. Alternatively, fraudsters may use either new accounts or existing accounts to move funds, such as by linking stolen credit cards or other compromised payment methods. Unauthorized access to accounts is often achieved through a range of tactics, including the AI-enabled phishing and social engineering schemes outlined above, leaving account holders unaware that their credentials are being exploited.

Proven strategies

Alternative financial services merchants need agile, intelligent fraud prevention strategies that can quickly adapt to new threats, identify anomalous behavior, and prevent false declines of good customers.

Especially as traditional KYC methods are becoming more vulnerable to fraud, financial platforms need the strongest possible anomaly detection downstream and the ability to make sound real-time decisions to apply friction with precision.

Tap into a network of intelligence

By analyzing different account types — first-time, new, and established — across legitimate and fraudulent transactions, FinServ businesses and trading platforms can better understand the unique challenges posed by each customer segment and tailor their risk management strategies accordingly.

In an industry like crypto, where new platforms are constantly emerging, the challenges are even greater. These platforms not only attract new customers but also lack years of historical data to identify patterns of legitimate or fraudulent behavior. Partnering with a company like Riskified can bridge this gap by leveraging a vast dataset of past transactions from a global merchant network. Even customers new to a platform often have an established history with other merchants within the network, offering valuable positive or negative signals that help create a more complete picture. This approach ensures that platforms can make informed decisions, even in the absence of their own historical data, and build trust in a rapidly evolving digital-first landscape.

71%

of customers new to cryptocurrency businesses were already part of the Riskified network

56%

of customers new to remittance businesses were already part of the Riskified network

74%

of customers new to precious metals businesses were already part of the Riskified network

Adopt adaptive strategies

Because fraudulent transactions and money orders are often executed in ways that mimic legitimate transactions, detecting masking tactics, such as the use of a proxy, is crucial for separating genuine transactions from fraudulent ones. Effective fraud prevention systems should also leverage anomaly detection to uncover irregular patterns.

Furthermore, robust identity clusters are an important method of identifying and blocking illegitimate orders. This requires a broad network of data with customer orders and claims across accounts and merchants, advanced machine learning models, and a clustering strategy for identity resolution and risk evaluation.

Partner with Riskified

Unleash growth with solutions designed to safeguard what matters most — your customers, their transactions, and trust in your business.

About our Risk Rundowns

Across industries, Riskified captures and analyzes data related to orders processed through our vast merchant network. We combine our findings with exclusive research and intelligence from online fraud forums and the dark web to provide merchants with category-specific insights.

Yael Hemo

Data Analyst, Data Insights team