Agentic commerce means detecting fraud with less data

It feels like every week brings a new headline or article about innovations in agentic commerce. As we move toward a world where AI agents conduct commerce at scale, clearly understanding the risks introduced becomes critical. One of the primary risks is the loss of key transaction signals used for fraud detection.

Categories of data

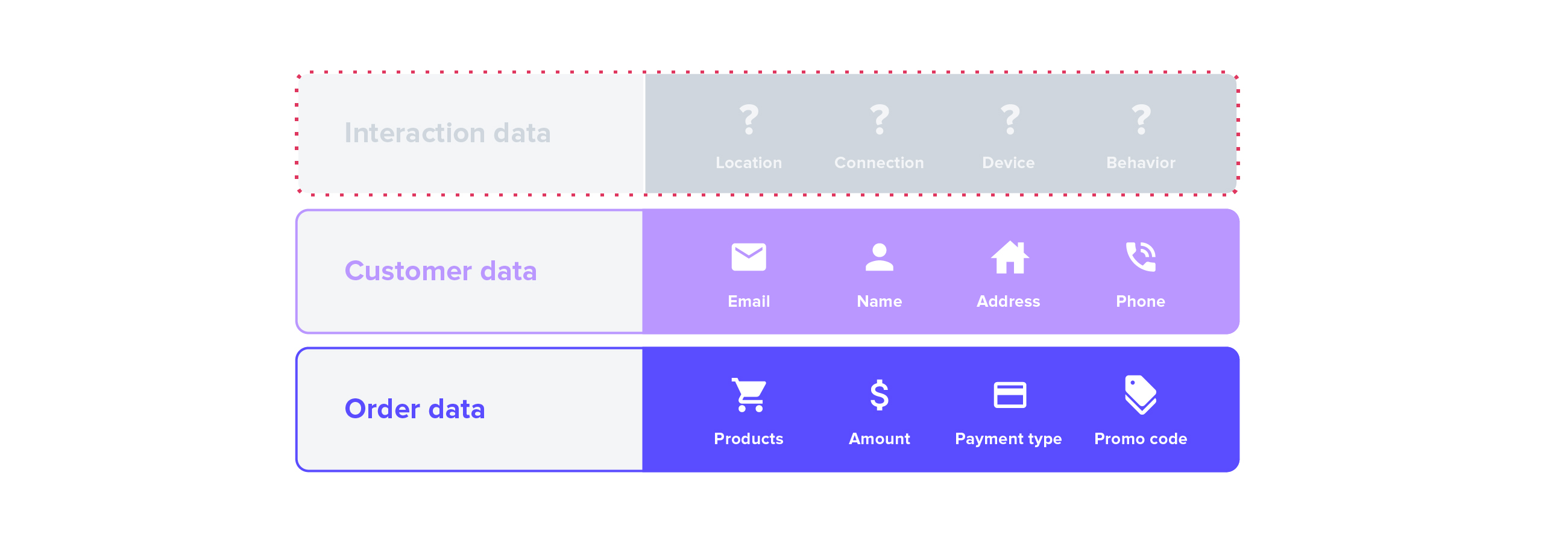

Typically, digital payment fraud detection analyzes multiple distinct categories of data to determine if a transaction is legitimate:

- Interaction data: Analyzes location, connection, device, and behavior to answer: “Is the user behaving like a typical customer?”

- Customer data: Uses email, name, address, and phone to answer: “Have you seen this customer before?”

- Order data: Examines the products, quantities, payment types, and promo codes to answer: “Are the products ordered attractive to fraudsters?”

Interaction data is vital because it informs systems of key details, such as the physical location from which the order was placed, the connection used (e.g., whether it is a public VPN), and device configuration comparisons, like the device time zone versus the IP geolocation country.

The agentic shift: Losing the “interaction” signals

The rise of agentic commerce disrupts this approach. When an agent enters transactions on behalf of the customer, a significant amount of data is lost in the interaction category.

Because a human isn’t physically tapping a screen or clicking a mouse, the system loses the ability to ask, “Is the user behaving like a typical customer?” The signals sourced from behavioral interaction, device fingerprinting, and connection analysis effectively vanish or become generic. This may significantly reduce the accuracy of fraud detection models.

What merchants can do to prepare

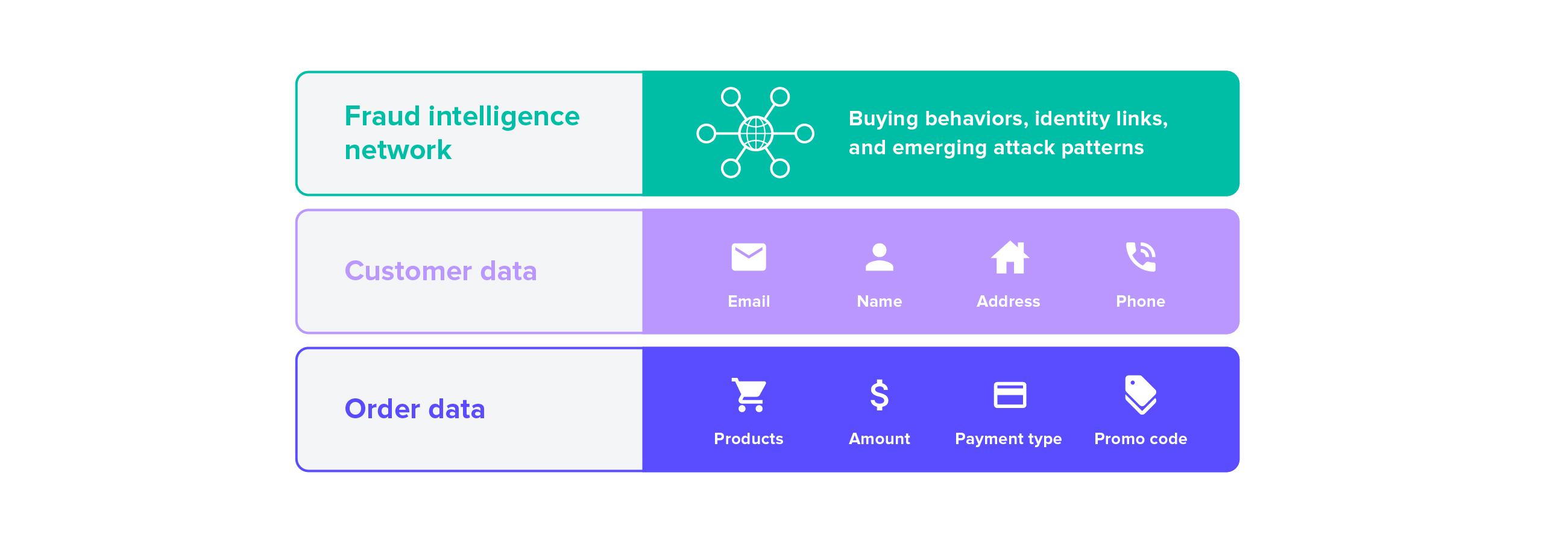

1. Leverage robust intelligence networks: Merchants must prepare for this loss of key signals. When interaction data is unavailable, tapping into fraud intelligence networks helps add the missing context.

A robust network supplements risk decisions made with less data by shifting the question from “How is this user interacting with my site or mobile app?” to “Has this customer or bad actor been observed across the intelligence network?”

Instead of relying on a single interaction, the network adds value in multiple areas:

- Buying behaviors: Data across the consortium helps determine if the agentic order exhibits typical or atypical behaviors.

- Identity linking: Systems can reference previous non-agentic interaction data to infer context on agentic orders.

- Pattern recognition: Networks identify emerging attack patterns that individual merchants might miss in isolation.

2. Identify agentic commerce transactions: Using a solution that can detect the signatures of agentic commerce transactions is not only important for fraud detection but also for reducing false positives.

Older generation solutions may have more rudimentary bot detection that can’t distinguish between an agentic commerce bot and a malicious bot developed by a bad actor. Solutions that properly identify the source of agentic orders can distinguish between legitimate AI bots and malicious ones.

3. Establish reporting and monitoring for agentic commerce transactions: Bad actors are known to probe new technologies for vulnerabilities to exploit. Ecommerce companies that see a significant spike in agentic transactions should have a plan to investigate the spike to ensure the spike is not related to a fraud attack.

Learn more about how Riskified can help with your agentic commerce strategy. Watch our latest webinar to explore the strategic shift required to combat AI-driven fraud.