The new returns reality

What do AI-assisted claims mean for ecommerce return policies?

As with most industries, AI is changing a lot about ecommerce — including how some consumers handle returns. That’s one of the more striking findings from Riskified’s 2026 report, “Rewriting the rules on returns,” which surveyed 2,091 consumers across seven markets and interviewed ten senior retail leaders at brands with revenues between $250 million and $10 billion.

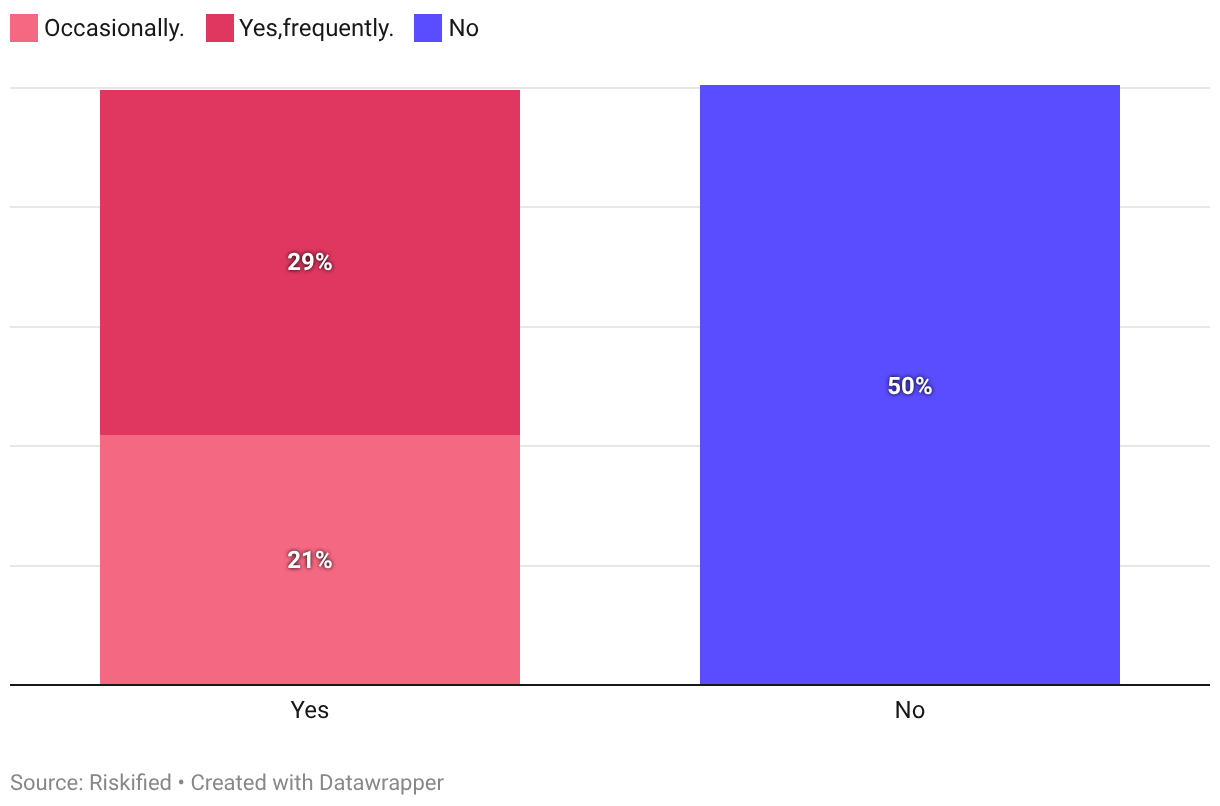

Nearly half of consumers have used AI to help with a return claim: The report found that 50% of consumers have used gen AI tools to help draft return or refund claims. That’s not a fringe behavior. It’s closer to standard practice.

To put it in context: Riskified’s 2025 agentic consumer survey found that between 32% and 49% of consumers across markets already prefer using AI to initiate a return or exchange. In less than a year, the direction of travel is clear.

Though what consumers are doing with AI ranges widely—from composing a clear explanation of a legitimate grievance to crafting a more persuasive account of what went wrong—the point isn’t that AI use is inherently abusive. For fraud teams, a well-written return claim is no longer a reliable signal of legitimacy.

Practitioners are seeing this play out in concrete ways. As one fraud operations leader noted in an industry forum: “We’ve been seeing cases where customers provide photos of damaged items that appear AI-generated or manipulated for claiming they received a damaged item. This has been happening for some time, but recently the volume has increased.”

Return abuse is getting easier to normalize, and social media plays a role

AI-assisted claims don’t exist in a vacuum. They’re part of a broader shift in how consumers think about returns. According to the report, 85% of consumers surveyed see at least some form of strategic or deceptive return behavior as normal. Only 15% reject all manipulative return practices outright.

Some of this shift is being driven by social media. A slight majority of global consumers (51%) have encountered return-related content on social platforms. Of those, 14% have used return “hacks” or strategies they found online, and 16% have both used and shared them.

But the influence isn’t uniform around the world. In China, nearly all consumers surveyed (93%) have encountered return-related content online, compared to just 40% in the US.

What merchants are doing about it

The retail leaders we spoke with are making concrete changes: narrowing acceptable return reasons, shortening return windows, and tightening quality checks on returned inventory. Several described shifting away from cash refunds toward store credit — retaining the money within their ecosystem to limit financial exposure from fraudulent claims.

But the merchants sharing the most nuanced perspectives were equally clear about the risk of overreach. As the Senior Director of Loss Prevention & Safety at a major specialty pet retailer told us: “The biggest thing that keeps policies from becoming very strict is that you do not want to alienate the honest customer and have that person pay the price for a bad actor.”

The practical response that emerged across multiple interviews: use data to distinguish between the majority of honest customers and those who are either angry or abusive. Then apply friction selectively rather than universally.

One merchant described a “step strategy” where risk levels trigger different decisions: reject the highest-risk claims, add disclosures for medium-risk cases, and quietly accept and track the lowest-risk ones. Another described adjusting return value thresholds specifically for consumers with a prior history of abusive behavior, without changing anything for the broader customer base.

As one risk professional put it in an industry forum: “This is a prevention problem more than a dispute problem…Return-before-refund rules, pre-dispute tools, and clear return terms help more than anything you send after.”

The broader takeaway

Even one year ago, a well-constructed return claim used to suggest a legitimate customer. That inference is now far less reliable. Behavioral history and identity intelligence—purchase patterns, prior return behavior, lifetime value—has become the more dependable signal.

The picture that emerges from the data isn’t a crisis. It’s a shift; one that rewards merchants who use behavioral data to help understand who they’re actually dealing with, rather than applying blanket responses to a problem that isn’t evenly distributed.

And, transparency also has a measurable effect. Riskified found that over 60% of consumers would adjust their return behavior if they knew the real costs of returns.