How to Communicate with Declined Credit Card Customers

A fraud solution that instantly approves good orders and reduces false declines can also greatly contribute to a positive customer experience. But even the most accurate fraud-detection systems aren’t correct 100% of the time, meaning that sometimes it’s your very own loyal, paying shoppers behind your declined orders. This makes it important that retailers pay attention to how they handle those declined orders. For some shoppers, what happens next is an important step in having a truly excellent customer experience. Before they can spread word-of-mouth damage to your brand reputation, communicate with declined customers to bring them back into the fold. Handling things well can reduce the number of angry complaints to customer service centers, and avoid the costs of losing legitimate, paying customers.

Turning lemons to lemonade – regaining the trust of falsely declined customers

When merchants communicate with declined customers, we recommend keeping three things in mind:

- Having your order declined is frustrating and possibly insulting. Shoppers wanted to spend money, and the retailer said no. Merchants should communicate with that in mind – clearly and to the point, without placing blame on the shopper.

- Help the customer understand the importance of fraud review. Declining fraudulent purchases benefits everyone (other than the fraudsters). Be sure to explain how legitimate cardholders benefit from proper fraud prevention.

- Offer a solution if you can. Consider suggesting shoppers use a payment method that doesn’t carry the same risks or gather additional information, such as an alternate phone number or email address, to reevaluate the transactions.

Credit Card Declined Sample Message

With all of that in mind, here’s an example of the type of message we recommend using to communicate a decline decision to a potentially high-intent customer:

Hello <SHOPPER>,

Thank you for your recent order with <MERCHANT>. We’re emailing to inform you that we are unable to fulfill that order, and your credit card has not been charged. We take security very seriously, and a major part of that is ensuring that orders are placed by the legitimate cardholder. This keeps our customers, other credit card holders and <MERCHANT> safe. Unfortunately, we were unable to verify this purchase, and it was declined out of caution. This is not a reflection on you as a shopper, and we apologize for the inconvenience.

We understand that you have a number of options when making a purchase, and we’re sorry for this frustration. We invite you to revisit <MERCHANT> and place your order again using details – such as phone number, email and billing address – that match the cardholder’s information. We will then re-evaluate it for fulfillment.

Thanks for shopping at <MERCHANT>.

That’s a starting point, and we recommend that merchants customize it to their liking, but it gives a sense of the approach that we recommend. Avoid blame, explain what happened, offer a solution, and make it clear and straightforward.

Keeping fraudsters in the dark – respectfully declining to accept fraud

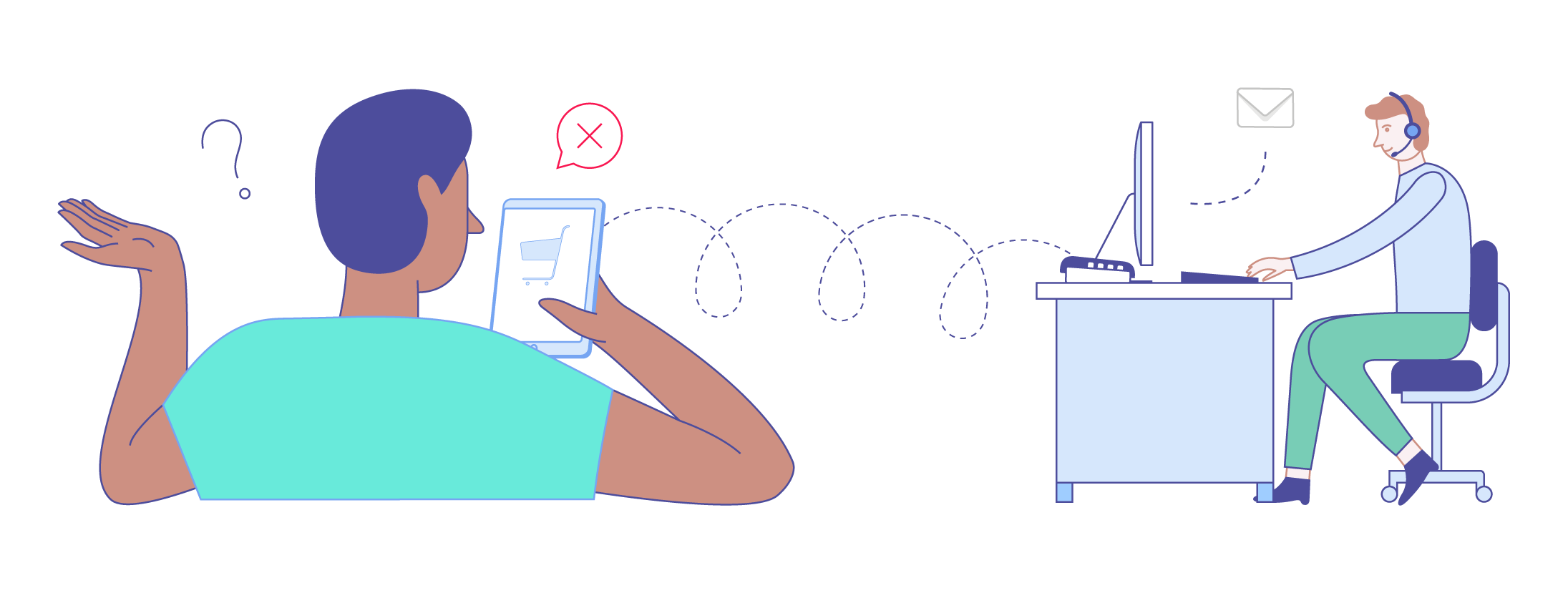

The other part to address, of course, is what to do for declined orders when you’re pretty sure they’ve been placed by fraudsters. This is a major reason behind the release of our “Decision Insights” tool, which explains how an order is reviewed for fraud. Some particularly brazen fraudsters will contact a merchant’s customer support team to overturn a decline. Even if unsuccessful, that fraudster may gain valuable information about why an order was declined and devise a workaround for future attempts.

That’s why we recommend that merchants keep clearly fraudulent declines at a healthy arm’s length. For these orders, it’s best not to provide a decline notification within the checkout process. Don’t email immediately after checkout to inform fraudsters of the decline. Give them a few hours or a day to move on to another target, and then inform them of the decline without providing a solution or additional details. Be polite! There’s no reason to upset them. But don’t give them cause to try again, either. Here’s our standard recommended reply for these cases:

Hello <SHOPPER>,

Thank you for visiting <MERCHANT>. We’re emailing to inform you that your recent order will not be completed.

We take security very seriously, and a major part of that is ensuring that orders are placed by the legitimate cardholder. This keeps our customers, other credit card holders and <MERCHANT> safe. Unfortunately, your order was deemed too risky and will not be fulfilled.

This is, again, only a starting point. Merchants should use whatever language feels right for them, but the general guidance remains the same. We’ve developed a document that lays out our approach to handling declines and includes messaging for specific situations. Merchants who have worked with us to refine their messaging have experienced significant reductions in the number of customer inquiries related to declines, freeing their teams from these time-intensive requests. That document is available to all Riskified merchants through their account manager or our customer success team.

Ultimately, the best defense against false declines is a fraud prevention solution that can accurately distinguish between legitimate and fraudulent transactions, helping you to approve more good orders while eliminating fraud risk. Talk to a Riskified fraud expert for more details.